Key Takeaways

- A new consumer tip from SCRS this week highlights that most people sign insurance policies without understanding the language — and it’s quietly costing them money.

- The average insurance policy is over 20,000 words long and written at a university reading level. Almost nobody actually reads it.

- Four specific sections — Definitions, Exclusions, Conditions, and Subrogation — are where most denied claims hide.

- An Indian consumer court just ordered an insurer to pay Rs 50 lakh (roughly $60,000 USD) because suspicion alone is not legal grounds for a denial.

- You can legally ask your insurer for a plain-language summary in many countries — and most people never do.

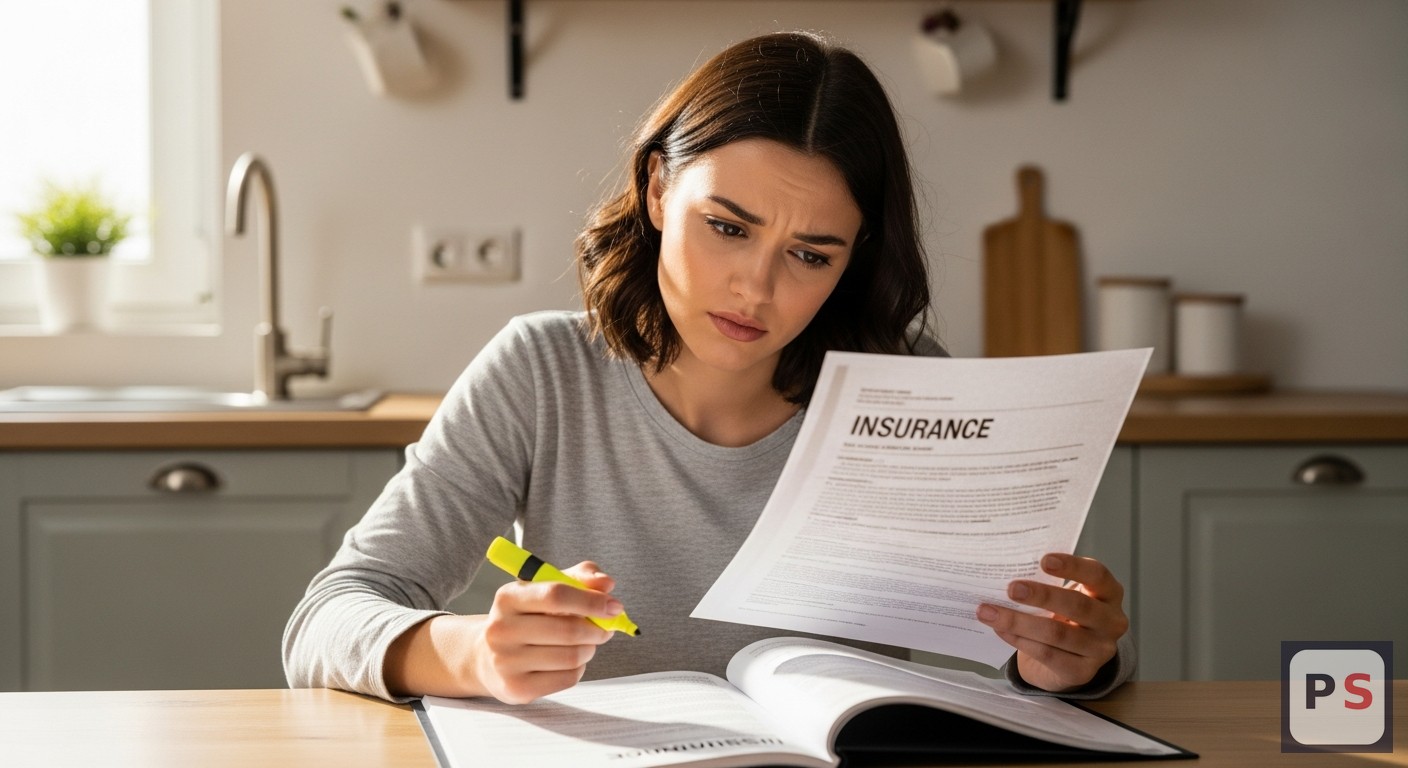

I came across a quick-tip bulletin published this week by SCRS — the Society of Collision Repair Specialists — and even though it was aimed at auto repair consumers, the core message hit differently. They basically said: most people cannot understand their own insurance policy, and the industry is not exactly rushing to fix that. I spent a couple of hours pulling on that thread, and honestly, what I found surprised me.

Let me walk you through exactly how to understand insurance policy language — because this week also gave us a genuinely shocking court case that proves the stakes are real.

Why Insurance Policy Language Is Designed to Be Hard to Read

Here’s a number that bothered me: the average car, home, or life insurance policy runs between 15,000 and 30,000 words. That’s about the same length as The Great Gatsby. And it’s written, on average, at a post-graduate reading level — according to a 2023 study published in the Geneva Association’s consumer literacy report.

So you’re not bad at reading. The document is genuinely hard. And that’s — well — convenient for the insurer.

The SCRS bulletin this week pointed out something sharp: when consumers don’t understand their policy language, they often accept whatever the insurer says without challenging it. They don’t know what they’re owed, so they don’t fight for it. Turns out, this is a global pattern. A 2024 World Bank report on financial inclusion found that in both high-income and developing countries, fewer than 30% of insurance holders could correctly identify what their policy excluded.

That 30% number stuck with me. I’m not sure I was in that group before this week.

The Four Sections That Actually Determine If You Get Paid

Most people skim the first few pages — the summary, the premium amount, the renewal date. That’s the friendly part. The part that determines whether a claim gets paid is buried much deeper. Here’s what actually matters:

Definitions. This is the most underrated section in any policy. Insurance companies redefine common words in ways that don’t match everyday language. The word “accident,” for example, is often defined so narrowly that a burst pipe or a weather-related event doesn’t qualify. If you ever file a claim and feel confused by the response, this section is where the fight starts.

Exclusions. This is the section that lists everything your policy does not cover. It can be 10 to 40 pages long on its own. Common exclusions that catch people off guard globally include: pre-existing conditions in health and travel insurance, “wear and tear” in home and auto policies, and events described as “acts of God” in flood or earthquake zones. These vary by country and insurer, but they’re almost always longer than people expect.

Conditions. This section explains what you have to do for the coverage to be valid. Report a theft within 24 hours. Submit documentation within 30 days. Notify the insurer before getting certain repairs done. Miss any of these conditions and a legitimate claim can be denied — technically legally.

Subrogation. This is the one almost nobody knows. It basically means: if your insurer pays your claim and it turns out someone else was responsible, your insurer has the right to sue that third party to recover the money. This matters because it can affect any settlement you might be pursuing independently. Most people find out about it the hard way.

The Court Case That Made This Real This Week

On the same day I was reading the SCRS bulletin, The Indian Express reported on a ruling from India’s consumer commission. An insurer had refused to pay a claim of Rs 50 lakh — roughly $60,000 USD — citing “suspicion of fraud.” The commission’s ruling was clear: suspicion is not proof. The insurer had no concrete evidence, just doubt. They were ordered to pay in full, plus compensation.

This case matters globally because it reflects a pattern consumer advocates have been flagging for years. In markets across Europe, Southeast Asia, and Latin America, insurers sometimes issue vague denial letters citing “policy conditions” or “investigation pending” without specifying what exactly is wrong. The assumption is that most consumers will accept the denial. Many do.

“Suspicion is not proof. An insurer cannot deny a legitimate claim simply because they have doubts without evidence to support them.” — India National Consumer Disputes Redressal Commission, June 2026

The practical takeaway here is not just for Indian policyholders. It’s for anyone, anywhere: if you receive a denial letter, request the specific clause number and section they are relying on. Vague denials that don’t cite exact policy language are often legally weak — but only if you push back.

- Você Pesquisa Autodesenvolvimento Todos os Dias, Mas Nada Realmente Muda — Aqui Está a Armadilha Oculta do Cérebro

- Melhorias Residenciais Dedutíveis nos Impostos Que Economizam Milhares — A Maioria dos Proprietários Está Completamente Perdida Nisso

- Amazon Prime Day 2026 Is Coming — And the Price Tricks They Use Will Cost You If You’re Not Ready

How to Actually Read a Policy Without Going Insane

I’m not going to tell you to read all 20,000 words. That’s unrealistic. But here’s what actually works:

First, ask your insurer for a Key Facts or Summary of Cover document. In the European Union, insurers are legally required to provide an Insurance Product Information Document (IPID) — a standardized two-page summary. In other regions, you may need to ask, but most insurers will provide one. This alone tells you the major exclusions in plain language.

Second, use the Ctrl+F (or search) function on digital policy documents. Search for “not covered,” “exclusion,” “shall not apply,” and “condition precedent.” These phrases are where the real limits of your coverage live.

Third — and this one is underused — call your insurer and ask them to explain the exclusions verbally. Tell them you want to understand what scenarios would lead to a denied claim. Some countries require insurers to answer this honestly. And even where it’s not mandated, most phone agents will walk you through it if you simply ask.

| Term | What It Sounds Like | What It Actually Means |

|---|---|---|

| Excess / Deductible | Something the insurer pays first | The amount you pay first before insurance kicks in |

| Subrogation | A technical legal term | Insurer’s right to recover money from a third party after paying your claim |

| Condition Precedent | An optional requirement | Something you must do or your entire claim can be voided |

| Market Value | What your item is worth | What it’s worth today — after depreciation, not what it costs to replace |

| Utmost Good Faith | The insurer being honest with you | Your legal obligation to disclose everything relevant — failure voids the policy |

🔍 Policy Confusion Score

Answer 6 quick questions to see how well you actually understand your own insurance policy — and how you compare to the average person.

1. Do you know what your policy’s excess (deductible) amount is right now?

How to Understand Insurance Policy Language When a Claim Gets Denied

If your claim is denied, here’s a process that works across most countries. Request the denial in writing — always. Ask them to cite the exact clause. Give them a deadline to respond, typically 14 days. If the response is still vague, escalate to your national financial ombudsman or consumer protection authority. These bodies exist in over 80 countries and most are free to use.

And remember what the Indian consumer court just reminded everyone this week: an insurer carrying suspicion is not the same as an insurer carrying evidence. You have more leverage than they want you to know.

The SCRS tip was really just a nudge. But sometimes a nudge in the right direction is all it takes to avoid losing thousands — quietly, invisibly, in the fine print you never got around to reading.

Last updated: July 02, 2026