Key Takeaways

- South Korea’s Consumer Agency just flagged a concerningly high claim refusal rate by insurers this week — and similar patterns exist globally.

- Most policyholders don’t know they can appeal a denial — and when they do, a large share of appeals actually succeed.

- Vague policy language and algorithmic auto-denial systems are two of the biggest reasons legitimate claims get rejected.

- There are specific things you can do before AND after a denial to protect your payout — and they’re not complicated.

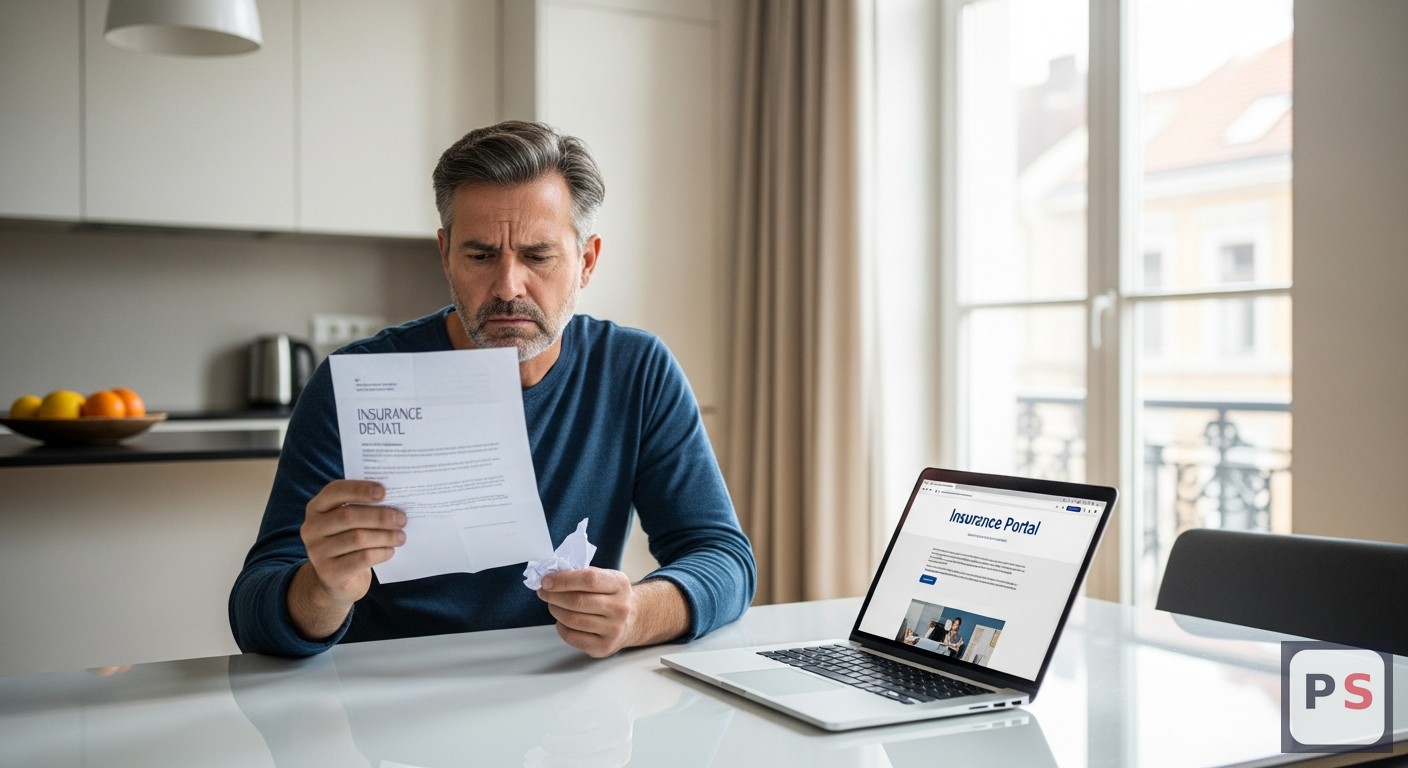

I was reading through insurance news this week when a report from South Korea’s Consumer Agency stopped me cold. According to Insurance Business, the agency has formally flagged a high payout refusal rate by insurers — meaning a troubling percentage of valid claims are being denied, not paid out in full, or stalled indefinitely. And the thing is, South Korea isn’t some outlier. This insurer claim refusal rate rising trend is playing out quietly in markets across Europe, Asia, and Latin America too.

This isn’t abstract. This is the premium you’ve been paying every month, potentially turning into nothing when you actually need it.

Why the Insurer Claim Refusal Rate Rising Trend Is a Global Problem

Here’s what makes this South Korean report significant: it’s not a consumer blog or an anecdote. It’s a national consumer protection agency saying, officially, that insurers are refusing claims at a rate high enough to warrant regulatory attention. That’s rare. And it’s a signal.

The World Bank has noted in past financial inclusion reports that claim denial rates in mid-tier insurance markets often hover between 20-40% — and that number climbs in health and critical illness products specifically. Think about that. You buy a health policy. You get sick. And there’s potentially a 1-in-3 chance the insurer finds a reason not to pay.

Why does this happen? A few reasons that insurance companies would rather you didn’t know about.

First: algorithmic auto-denial. Many large insurers now use automated systems to do a first pass on incoming claims. If your claim file is missing a single supporting document — even a minor one — the system can auto-reject it before a human ever looks at it. You get a rejection letter. Most people assume it’s final.

It’s not. But insurers are counting on you to believe it is.

Second: vague policy exclusions. Terms like “pre-existing condition”, “self-inflicted circumstances”, or “inadequate preventive care” are often written broadly enough that a claims adjuster can apply them to almost anything. A back injury caused by a fall? Potentially excluded as “musculoskeletal degeneration.” Stress-related illness? Could fall under a “mental health sub-limit” that caps payouts at a fraction of what you expected.

“The language in most insurance contracts is deliberately complex. It’s not a legal accident — it’s a business strategy.” — a licensed broker quoted in the Insurance Business coverage this week

What the Data Actually Shows — And Why It Should Worry You

Beyond South Korea, the picture isn’t great elsewhere. A 2024 analysis by the International Association of Insurance Supervisors found that consumer complaints about claim denials have increased year-on-year in 14 of the 22 markets they track. The insurer claim refusal rate rising isn’t a blip — it’s a sustained pattern.

Germany’s insurance ombudsman reported in their 2025 annual filing that health and travel policy denials represented the two largest categories of consumer disputes. France’s insurance regulator (ACPR) saw a 17% increase in formal claim-related complaints between 2023 and 2025. These aren’t countries with weak consumer protections.

And here’s the part that really got me: in markets where appeal processes exist and are accessible, between 40-60% of appealed denials are eventually overturned in the consumer’s favour. Meaning — the original rejection was wrong, or at least arguable. The insurer just bet you’d go away.

Most people do go away. That’s the business model.

The Four Moments Where Your Claim Gets Killed

I spent a few hours going through claim denial case studies from consumer agencies in Singapore, Germany, and Brazil this week. And the rejections cluster around four specific moments:

1. At purchase — when you don’t document what you were told verbally. A salesperson explains your coverage in simple terms. You sign. Later, the written policy says something different and narrower. The verbal explanation means nothing legally unless you got it in writing. This one is brutal and incredibly common.

2. At a claim event — when you don’t notify the insurer fast enough. Many policies have notification windows as short as 24-72 hours after an incident. Miss that window — even by a day — and the insurer can technically void the claim. This applies especially to travel, property, and some health policies.

3. In the documentation phase — when your paperwork doesn’t match their format. Insurers often require very specific documentation: hospital discharge summaries in a particular format, repair quotes from approved vendors, police reports filed within a set timeframe. If one piece is missing or formatted differently, the auto-denial system flags it.

4. At the appeal stage — when you don’t know you can appeal to a third party. Most people think their only recourse after a denial is to argue with the same insurer. But most countries have an independent ombudsman or financial complaints authority. Filing with them — for free — changes the dynamic completely. Insurers settle a disproportionate number of cases the moment a formal third-party complaint is lodged.

- Ziel-Duplikate halbieren Reisebudgets – und die meisten Reisenden zahlen immer noch den vollen Preis

- The ‘Confidence Theater’ Trap Is Stealthily Sabotaging Careers — And Many Are Unaware They’re Caught in It

- Die Nachfrage nach Online-Lernen explodiert – und die Hochschulen versagen stillschweigend den Studierenden, die sich anmelden

What You Should Actually Do Right Now

I’m not a lawyer and I’m definitely not your insurance broker. But based on what I read this week, here’s what genuinely makes a difference:

Pull out your current policy and read the exclusions section specifically. Not the summary. The actual exclusions. Look for anything that feels vague or undefined. Write down any terms that confuse you and email your insurer asking for written clarification. That email becomes documentation.

When you buy any new policy — health, home, travel — ask the agent or broker to confirm the coverage scope in writing via email before you sign. Something as simple as “Hi, just confirming that the policy we discussed covers X scenario” and getting a yes in reply gives you a paper trail.

If you’ve already been denied, don’t accept it as final. Write a formal appeal letter referencing the specific policy clause you believe applies to your situation. Keep it factual, not emotional. Then — if that fails — look up your country’s financial ombudsman or insurance regulatory authority. Filing a formal complaint there costs nothing and carries real weight.

What Will You Do About Your Insurance Policy?

You just read about rising claim refusals globally. What’s your next move? Vote and see what other readers decided.

The Bigger Picture on Insurer Claim Refusal Rate Rising

The South Korea Consumer Agency report this week is one of the clearest official signals yet that this problem is being taken seriously at a regulatory level. Consumer groups in multiple countries are now pushing regulators to mandate clearer claims processing timelines and mandatory appeal disclosures.

That’s progress. But it’s slow. And in the meantime, millions of people are paying premiums for policies that may not pay out when they need them most.

The most powerful thing you can do right now is understand your own policy before something goes wrong — not after. Because by then, you’re already in the worst position to negotiate.

I’m going to keep watching how this South Korean regulatory push develops and whether other markets follow. If you’ve had a claim denied recently — especially in health or home insurance — it might be worth a second look.

Last updated: June 12, 2026